Blog Post

Modeling Cyber Resilience Is Now a Regulatory Priority

July 29, 2025

TL;DR

- The ECB is requiring banks to simulate how systemic shocks such as cyber attacks, geopolitical conflict, and dollar shortages could impact their capital reserves.

- Supervisory expectations are shifting away from control checklists and toward data-backed modeling of institutional risk exposure.

- By naming cyber alongside traditional macroeconomic threats, the ECB is explicitly signaling that digital disruption carries market-wide consequences.

- CISOs, CROs, and other executives are under growing pressure to align on impact scenarios and communicate risk in business terms.

- Cyber risk quantification (CRQ) provides the modeling capability, financial clarity, and operational insight needed to meet these emerging regulatory demands.

A New Level of Supervisory Expectation

The European Central Bank (ECB), tasked with maintaining financial stability in the region, is changing how it supervises institutional resilience. According to a July 2025 Reuters report, banks across the Eurozone are being asked explicitly to model how large-scale disruptions, including geopolitical conflict, potential dollar shortages, and cyber incidents, could impact their capital reserves.

The request marks a notable shift in supervisory expectations. Instead of reviewing technical controls or verifying compliance, the ECB will now press banks to demonstrate an unequivocal understanding of their exposure and the ability to forecast the financial implications of severe, real-world scenarios. While frameworks including DORA already require financial entities to test digital resilience, this latest directive signals a deeper focus on capital-level consequences.

The updated ordinance is also a step toward embedding risk modeling into the core of regulatory oversight. Although it only applies to certain European banks, the message extends well beyond the financial sector. As the consequences of systemic risk grow more damaging, leaders are being requested to discard the abstract threat language and prepare for a new standard that prioritizes data-driven insights over assumptions, and preparation over posture.

Risk Modeling Becomes a Mandate

Historically, ECB supervisory reviews have centered on whether financial institutions have adequate controls in place, including firewalls, incident response plans, redundancy systems, and the like. These reviews emphasized the importance of safeguards, but rarely interrogated how effective they would be in the face of large-scale, multi-vector disruptions. Risk management, in this context, was thus treated as something that could be documented, but not necessarily modeled.

The ECB's new ambition directly challenges that approach, starkly communicating that institutional resilience will no longer be measured by the presence of policies and controls alone. Significant banks are now expected to simulate how specific scenarios could degrade their capital position, allowing stakeholders to assess not only the immediate impacts of an event but also the downstream financial and reputational outcomes.

In practical terms, the objective is that entities will be able to articulate, in clear business-aligned terms, how adverse events would affect them. Moreover, they need to have a credible understanding of which functions are exposed, what the financial losses might be if those functions or relative assets were compromised, and how long a potential disruption would last.

Declaring Cyber as a Macroeconomic Vulnerability

Cyber risk has famously struggled to secure the recognition matching that of other macroeconomic threats. Despite a growing awareness that cyber events have the capacity to render an organization insolvent, they still often remain framed by senior stakeholders as technical challenges, leaving respective issues isolated from the rest of the enterprise risk management strategy and excluding them from financial stress testing.

Only lately has that framing begun to evolve. By including cyber incidents on the same list as geopolitical conflict and dollar shortages, the ECB is overtly acknowledging that cyber risk doesn't stop at the perimeter, a fact that many cybersecurity experts have known for years. On the contrary, it rapidly diffuses through vendors and internal systems, housing the potential to trigger cascading effects that institutions are rarely equipped to quantify in actionable terms.

The inclusion of cyber also reflects the current geopolitical reality. Banks operating in regions vulnerable to state-aligned threat activity, for instance, face persistent targeting that mere internal defense mechanisms can't mitigate, as exposure is often embedded in national-level infrastructure. Without knowing how these dependencies translate into business risk, teams are left managing assumptions. In naming cyber risk alongside these other, more customary threats, the ECB is explicitly recognizing digital resilience as essential to market stability.

Strategic Pressure on CISOs and Risk Leaders

As the ECB's regulatory expectations expand, new pressures are being created specifically for those executive leaders charged with managing risk oversight. On top of their already long list of responsibilities, chief information security officers (CISOs), chief risk officers (CROs), and their counterparts will be evaluated on how well they can understand and articulate the impending effects of a potential failure in financial, operational, and reputational terms alike.

This new level of expectation will shift the dynamic in many organizations, requiring previously siloed stakeholders to align closely with one another, building a shared visibility into exposure and jointly defining which events deserve prioritized attention. Boards, similarly, don't need assurance that everything is "under control," but rather a realistic picture of what's at stake and whether preparation matches that level of risk. With the ECB's new mandate, institutions are expected to tangibly understand their losses and take action well before an incident occurs.

Cyber Risk Quantification as an Imperative for Capital Risk Readiness

To meet the ECB's elevated demand for capital-level risk forecasting, institutions must adopt new tools that are capable of modeling exposure with rigor and precision. While cyber risk quantification (CRQ) solutions were already gaining traction in the market due to their ability to facilitate cross-department collaboration, their core analytical engine has now become a strategic asset in its own right, central to meeting these latest regulatory mandates.

Unlike traditional maturity assessments or qualitative score frameworks, CRQ solutions perform an inside-out scan to capture an organization's real infrastructure. They also automatically account for the institution's unique threat landscape based on its geography, industry, and revenue band and leverage control maturity as inputs to simulate how specific scenarios, such as ransomware attacks, third-party breaches, and operational outages, could translate into financial loss.

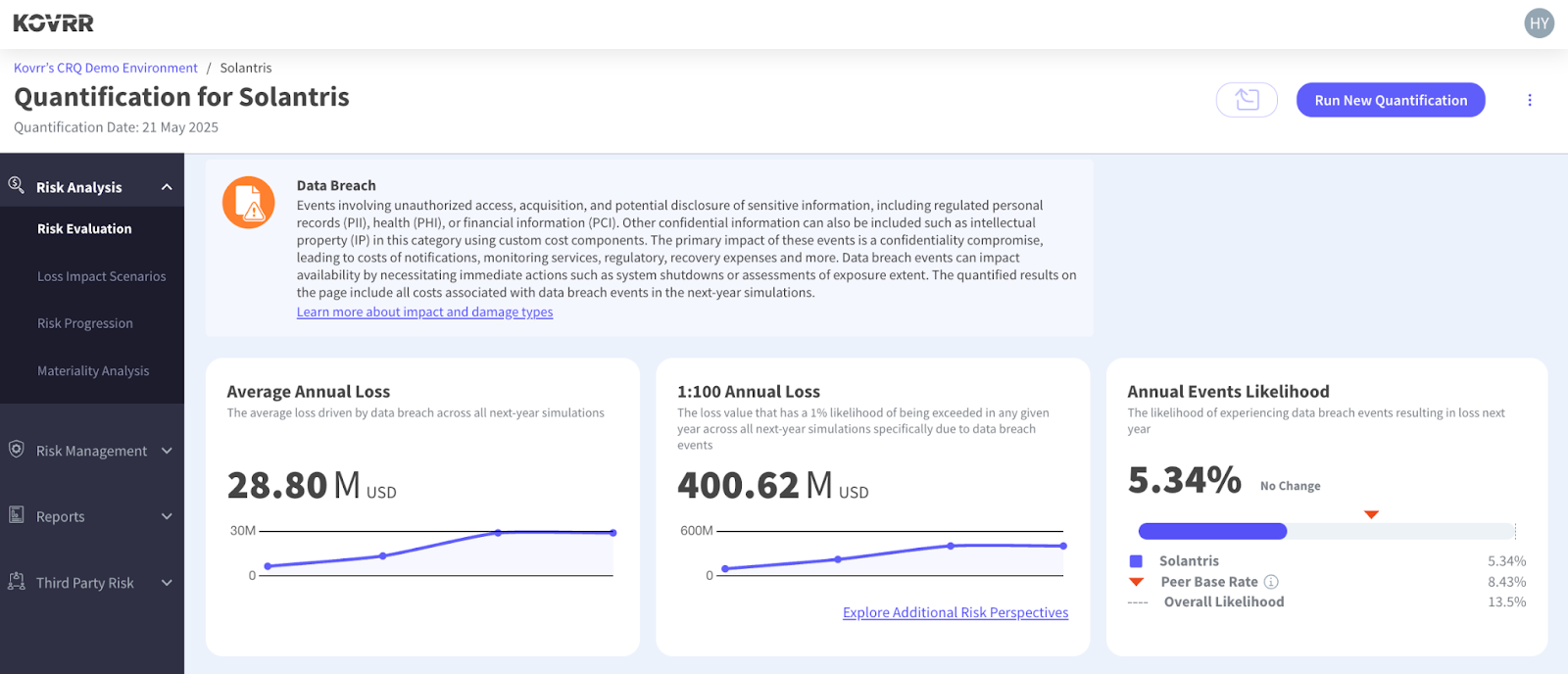

For example, in Figure 1, the CRQ model simulated next-year data breach scenarios for the financial institution "Solantris," and found that, while the average annual loss (AAL) is forecasted at $28.8 million, there is also a 1-in-100-year event that could amount to $400.6 million of loss, a figure even more critical when evaluating whether existing capital buffers and cybersecurity insurance coverage are sufficient.

More importantly, the annual event likelihood of 5.34%, notably lower than the global peer benchmark, can inform Solantris's stakeholders on how to optimally allocate resources. With the clear, quantified information, leadership may determine that existing controls are effective enough to maintain the current budget, or conversely, that the concentration of loss in a few extreme scenarios justifies resource reallocation toward prevention or incident response measures.

With CRQ, cybersecurity investments can also be assessed through projected ROI, loss scenarios tied to business services and mapped to insurance coverage, and board reporting delivered in the same financial terms used for credit or liquidity risk. This level of specificity shifts cyber planning from abstract threat awareness to quantifiable exposure management, equipping CISOs, CROs, and other risk management leaders to meet the ECB’s expectations for capital-focused, forward-looking risk oversight.

Operationalizing CRQ for ECB Scenario Management

While CRQ seamlessly delivers the financial clarity and modeling rigor regulators now expect, organizations still need a means to operationalize and maintain that insight across evolving scenarios. With Kovrr's one-of-a-kind quantified cyber risk register, teams can continuously update and manage ECB-relevant loss scenarios with live threat intelligence, control posture, and financial modeling logic drawn directly from Kovrr's CRQ engine. The register also doubles as documented proof that scenario-based modeling is both active and defensible.

From Regional Supervision to Global Signal

The ECB's scenario-focused directive is a part of a growing pattern in explicit regulatory supervision. Authorities worldwide are revisiting how cyber risk ought to be defined, managed, and communicated to both the public and necessary governing bodies. The US SEC's cybersecurity disclosure requirements and the implementation of NIS2 and DORA in the EU, for instance, all reflect a shared expectation that organizations need to quantify potential cyber disruptions and articulate the financial impact in board-ready terms.

Although these specific cybersecurity frameworks differ in scope, they converge in their demand for forward-looking risk practitioners. They and many of their national equivalents require that organizational stakeholders anticipate the scale of loss in advance and prepare accordingly, a directive that has grown more urgent amid the rise of systemic events like the July 2024 Crowdstrike outage, which spread rapidly across interconnected infrastructure and markets.

Institutions that begin adapting to these expectations now, even those that fall outside of the purview of the ECB's mandate, by investing in credible scenario modeling and strengthening internal alignment, will be better positioned to meet the next wave of requirements that will inevitably come. The ECB's move offers an obvious signal to those paying attention, not only for Europe's financial sector but for all entities operating within complex, digitally dependent economies that the need to demonstrate measurable preparedness is coming.

Supervisory Readiness Now Demands Quantification

The ECB's announcement marks a pivotal shift for the way cyber risk is perceived, conveying that it sits squarely alongside credit, liquidity, and geopolitical threats as a driver of institutional fragility. Such an unambiguous elevation, likewise, reflects a broader acknowledgement that digital disruption poses systemic consequences and must therefore be governed with the same analytical rigor and methodologies as other forms of regulated enterprise risk.

Ultimately, executive leaders must be prepared to articulate, in financial and operational terms, where cyber risk resides within their organization, how it could materialize, and whether or not current strategies are sufficient. Generalized assessments and abstract maturity scores are no longer enough to satisfy regulators. What's necessary, instead, is modeled exposure simulations, mapped to an organization's infrastructure and backed by data-driven logic.

Meeting that expectation is exactly what cyber risk quantification enables. CRQ models are a straightforward mechanism for translating the technicalities of cyber risk into tangible business outcomes, empowering leadership to not only communicate exposure in the classic language of enterprise oversight but also prioritize mitigation initiatives with precision. While the ECB may be the first regulator to formalize this expectation, it will certainly not be the last, and the organizations that adapt now will be the ones best equipped to endure what comes next.

If your organization needs to start running scenario-based cyber risk modeling and communicating exposure in financial terms, book a free demo of Kovrr’s CRQ platform today.

.webp)